I’m a little surprised people are still studying this, since it’s been studied before with the same results:

After 12 weeks, researchers found no meaningful differences in weight gain, body composition, or cholesterol levels between people following the low-dairy diet and those eating three servings of dairy each day. Participants consuming more dairy, however, showed improvements in blood pressure and consumed more calcium, protein, and vitamin D.

“Those that had three servings of dairy didn’t have adverse levels of blood cholesterol or lipids or evidence of insulin resistance,” says Anderson.

I would argue that that full-fat dairy is “minimally processed.” (Mixing the milk of multiple cows, pasteurizing, and homogenizing, means it’s not unprocessed.) I argue that skimming off half (or nearly all) of the fat crosses the bar to “processed,” but even if you don’t draw that line where I do, it’s still more processed. And just on general principles, I generally assume that less-processed food is better than more-processed food.

But with full-fat dairy you don’t have to go by general principles. We have multiple studies over years and years that show unequivocally that it’s healthier food.

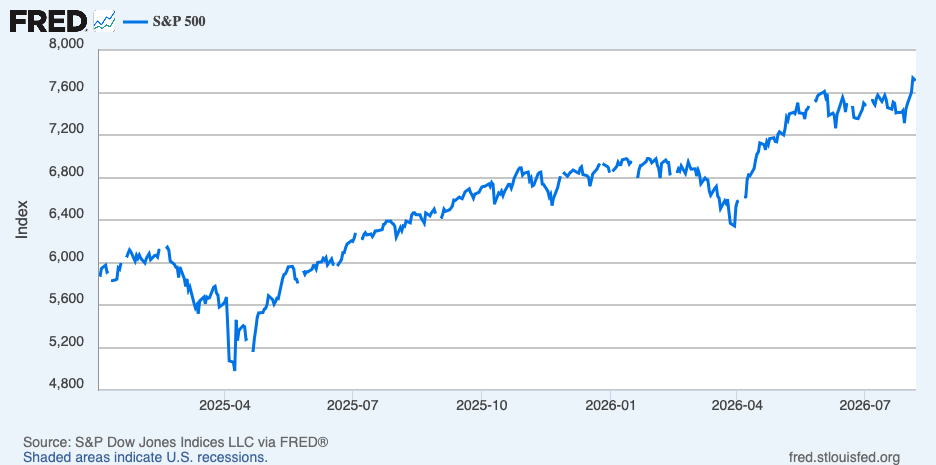

If, like me, you had any sort of reasonably balanced portfolio at the beginning of the year (or the beginning of last year), it’s worth observing that it is almost certainly way, way out of balance.

If so, this is your reminder to rebalance your portfolio.

Doing so is admittedly really hard to do. If you had a 60:40 (stocks to bonds) portfolio at the beginning of last year, you might very well have 70% or 80% invested in stocks now, and that probably feels great. You feel like a genius, letting your profits run. If there’s anything better than having 60% of your portfolio grow at 20% a year it’s having 80% of your portfolio grow at 20% a year.

But you know it’s a terrible idea. It’s bad enough to have 60% of your portfolio lose half its value. Having 80% of your portfolio lose half its value is much, much worse.

Knowing that it’s hard, let me point out a little thing that might make it a little easier right now: Bond rates are up nicely. You can get nearly 5.25% on 30-year bonds, or almost 3% on inflation-adjusted bonds. That’s good enough that you don’t really need to agonize about whether you can expect a capital gain or capital loss on the bond. Just buy it and take the coupon.

Of course, I have no idea what balance is right for your portfolio. Maybe it’s 60:40. If you’re young, maybe it’s 80:20. If you’re retired, maybe it’s 35:65. But if you had a sensible balance a year or two ago, and you haven’t rebalanced, it is now way out of whack.

Light exposure is good for you. All the different frequencies are good for you. This has led many people to try to tweeze them apart: tanning beds, red-light panels and masks, therapy lights, etc. It turns out, sunlight is best consumed whole, just like food.

I should mention that by inclination, I’m rather vulnerable to getting this wrong. I wrote at some length about how, because of the sort of person I am, I simply like the idea of figuring out all the nutrients I need, and then trying to construct a diet that provides all those things. Similarly, I like the idea of coming up with a perfect workout plan, and then getting all the movement that I need by hitting all the right exercises. But, if you follow that link, you’ll see that I eventually realized the whole notion was just wrong-headed.

There is no need—in fact, no value—in tweezing apart the nutrients in food. Just eat a varied, whole-food diet and your body will get it right. The same with movement. Just engage in a wide range of diverse movement, and your body will become highly capable of moving in all those ways, (and if your “movement diet” is adequately diverse, your body will become fairly capable of all sorts of movements you don’t even practice).

The book is consciously modeled on Michael Pollan’s In Defence of Food, which systematically destroyed the notion that you could build up a diet that optimized all the nutrients. And it’s message is very similar. Sunlight is best consumed whole, just like food.

All of the different frequencies are good for you:

UV (to make vitamin D, and to release nitric oxide from the skin into the blood),

blue (to tell your brain it is daytime, and to tell your subcutaneous fat cells to release fat and signal your brown fat to burn it for energy),

green and yellow (to calm you down—I have written before about my theory of dappled shade, and for vision—you see shades of yellow better than shades of white, which is why yellow glasses are good for driving, shooting, and the like),

red light and infrared light (to boost energy production in your mitochondria and promote wound healing).

“But what about skin cancer!?!?” I can hear you asking from here.

The book is well worth reading, because just the information on skin cancer is worth the price of the book (and it takes half the book to adequately deal with the subject). Because there’s so much of it, it’s not really practical to try to summarize it here, so I’ll just mention that “Don’t get sunburned” is much better advice than “Put on sunbock,” or even “Stay out of the sun.”

I figured this out years ago. I’ll use sunblock if I’m going to be out in the sun so long that I might get sunburned—I needed it for a snorkling trip to Buck Island, for example. Otherwise, I use a combination of changing my clothes, taking advantage of shade, and limiting my time out in the midday sun. But I don’t minimize my time in the sun. I maximize my time in the sun, while making sure not to get sunburned. At this point in the summer (having gotten a modest amount of sun every day since the weather turned warm) I’m okay for up to about 40 minutes of mid-day sun. And I try to get that nearly every day.

Here’s one statistic, that I’ll let stand in for dozens of others about the advantages of sun exposure. The UK Biobank has data on health outcomes for hundreds of thousands of people. A researcher Jacobsen mentions went in and counted:

… in the fifteen years of tracking, a total of 40 people had died from skin cancer attributable to too much UV light, while 2,982 people had died from diseases attributable to a deficiency of sunlight.

The final third of the book is about artificial light, and makes the case that too much light at night is just as bad as too little light during the day.

Again, this is something that I figured out long ago. All the “sleep hygiene” stuff makes it clear that you want your sleeping space to be very dark, and there’s no doubt that getting enough high-quality sleep is probably the best thing you can do for your health, maybe even above good nutrition and plenty of exercise (both of which are easier to get if you’re sleeping well).

The prescription is almost trivially easy: Get outside at dawn. Get as much sunlight as you can without burning during the day. Within a couple of hours after sunset make your space as dark as possible and get some sleep.

A guy I follow on micro.blog, after having to go through four or five steps just to read a Substack post, posted “Substack? What are you for?” To which I replied: “As near as I can tell, it’s there to monetize the writing of Nazis, with enough non-Nazis to provide some cover for the firm.”

My brother chimed in to point out, “You can subscribe to nazistack blogs with an RSS reader,” which is something that I hadn’t really thought about.

I’ve been avoiding any newsletter on Substack for a couple of years now, because of the “Nazi bar” problem. Even so, I’ve ended up with a couple of subscriptions to Substack newsletters, because a couple of non-Substack newsletters I subscribed to moved there, and Substack let them just subscribe me without asking. And because I wouldn’t have subscribed if I wasn’t interested, I didn’t unsubscribe from every one of those.

Now, though, based on Steven’s good idea, I’ve gone in and added those newsletters to my RSS feed. Now I can unsubscribe from those newsletters, and still see their content—in my feeds, which is the best place to see it anyway!

AI firms are on the ropes, having spent way too much money building infrastructure for tools that are valuable, but not nearly valuable enough to support the money already spent, let alone what they’re planning to spend over the next two or thee years. This is bound to come to a bad end.

As Jerry Holkins puts it:

They can only loan each other money for so long. Then, they’ll socialize the losses through nationalization.

At least, that’s their plan. Oliver Jutel and Gil Duran have a name for this plan: “exit through the state.”

Because I’m at heart an optimist, I like to imagine a more hopeful solution—one where this plan fails. And I legit think it might.

If Congress changes hands, and Trump becomes even more toxic (two things that seem very likely), there might not be anybody in a position to lead the charge for socializing the losses. A toxic Trump trying to hand another bunch of taxpayer money over to billionaire tech bros might actually be very unpopular. And if a Republican minority in Congress can’t get it together to come up with a plan that a significant number of Democrats will support, socializing the losses just might not happen.

But it has to “not happen” right then—with a Democratic (or divided) Congress.

If the AI firms can hold things together (with circular financing, SPVs, and the like) until there’s a Democrat in the White House, that guy will probably not be able to resist the pressure to “do something.”

If—as I hope, and kind of expect—it comes to a head before that, the Republicans might well not be able to come up with a plan that meets the demands of all their different constituencies, while the Democrats refuse to join in any plan that a large subset of Republicans will agree to. The result might just be that we just let the sucker go down.

Letting the sucker go down is what George W. Bush wouldn’t do in 2008. Except, of course, he kinda did, as far as homeowners were concerned. Banks, investment firms, and insurance companies got saved. Homeowners got hung out to dry.

My point being that the government is totally willing to let some suckers go down. The Republicans would like those suckers to be ordinary investors, computer users, and (in particular) tax payers. But I like to imagine that there’s at least some chance that the politicians will simply be unable to cobble together an arrangement to accomplish that, with the result that the AI firms go down, a bunch of AI firm executives get prosecuted for investment fraud, and all that infrastructure (data centers and large language models) gets sold off in bankruptcy, ending up in the hands of people with a certain amount of rationality (and much less debt).

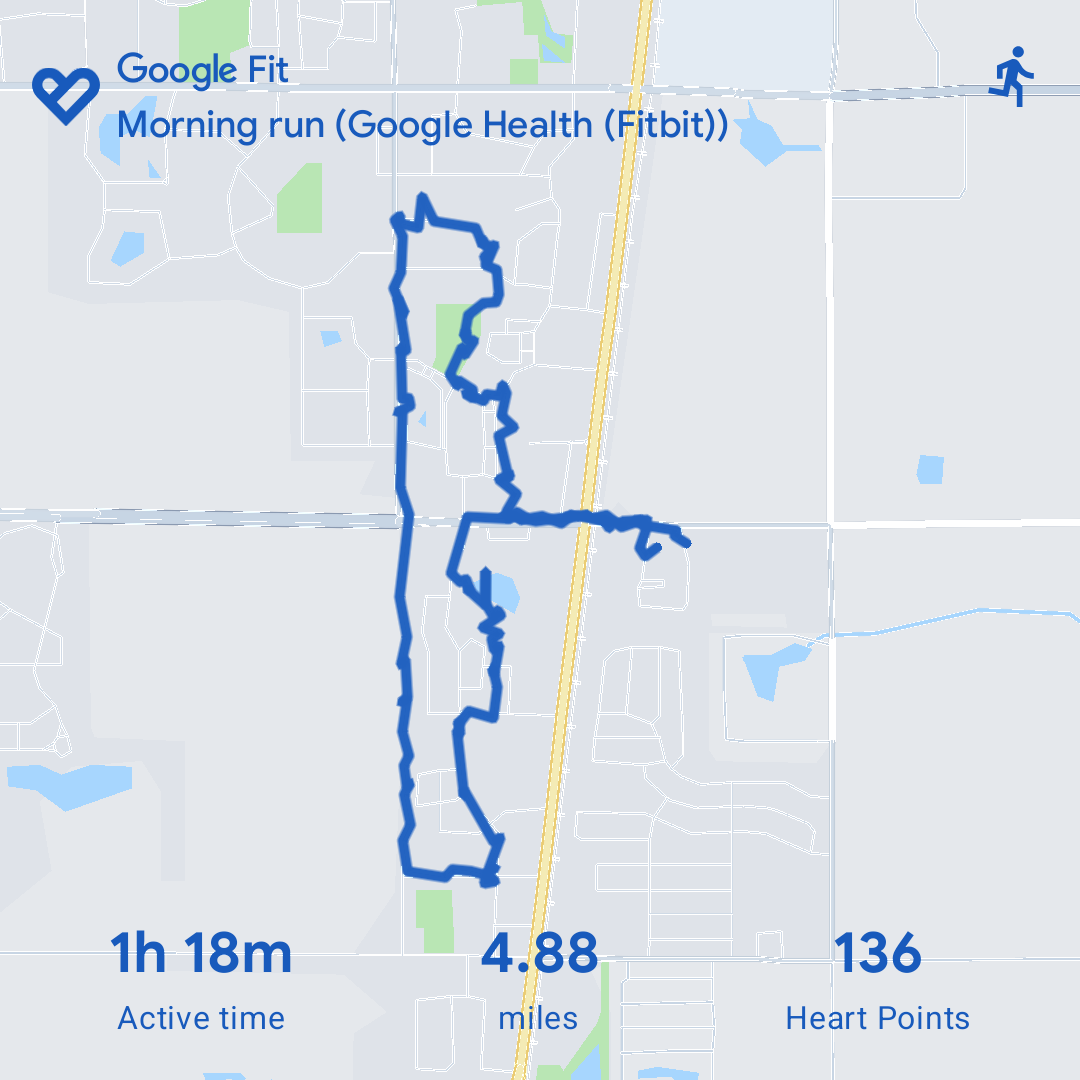

It was a very nice day today—moderate clouds, not too hot, no rain—so I decided to go for a run.

I haven’t actually compared it to other runs this summer, but I’m pretty sure it’s my longest and my fastest.

4.88 miles in 1h 18 min.

I really mean to do two runs a week, but I’m probably not managing even half that. But this run still felt okay. I was tired at the end, but not too tired. My joints felt fine during the run.

A few weeks ago, back before the Iran war heated back up, The Economist wrote a mia culpa, explaining why they’d gotten it wrong about the war being an economic disaster. Briefly, while the MOU was holding up, I was tempted to write my own.

I didn’t write a mia culpa. To be fair, part of that was just laziness. But part of it was looking at things and thinking I was still right. Maybe between some demand destruction and some dribs and drabs of oil getting through the strait, world markets had found a new equilibrium that wasn’t nearly as bad as I’d expected. But I didn’t think so.

The Economist thought so. They thought they’d gotten it wrong for two reasons:

First, we thought that America and Iran would hold out against a deal to reopen the Strait of Hormuz: America because Mr Trump deludedly thought he held the whip hand, Iran because its regime knew its people could be made to endure more pain. In fact, facing the fury of American motorists, Mr Trump all but folded, preventing a disaster. Since the two parties struck a provisional deal in June, enough oil has been getting out of the Gulf to reassure markets that supply is coming back online, even if the future of the strait remains uncertain.

Our second oversight was, like others, not anticipating the staggering degree to which China would be able to slash its oil imports. Crude imports are 5m barrels a day lower than a year ago, despite the fall in prices. China has cut its demand and shored up supply. Its oil reserves are opaque—many barrels are hidden from satellites underground, and there is a blurred line between official reserves and corporate inventories. But they have been shown to be a powerful buffer.

I pretty much bought their second point. China had produced a truly fantastic amount of demand destruction, and had done it with minimal impact on their own economy, by largely shifting the impact onto people in other countries who had bought their oil distillates, before China prohibited exports. They could probably keep that up indefinitely, removing their demand from the world market.

That first point, though, I found doubtful. I mean, yes, Trump always chickens out, which is why we got the MOU and the briefly partially reopened strait. But I think they were wrong in thinking that Iran would go along with what Trump wanted, or that Trump could settle for what Iran would (obviously) want to do. They tried to paper over the cracks for a few weeks. I mean, I believe Trump settling for whatever Iran did and pretending it was a victory was a thing that could happen. But I’m not surprised it didn’t work out. Too many other people in the U.S. government were simply unwilling to let Trump leave the strait in Iran’s hands. And, although oil prices were coming back down, they were not on a trajectory that would improve the Republican’s chances in the midterms.

So, I think The Economist was right in the first place, and wrong to imagine that Trump and Iran could agree that “preventing a disaster” was something they could do.

The oil price graphic above is already out of date. It shows yesterday’s closing price, and things have gotten worse already today. Brent crude is over $100 as I wrap up this post.

On Saturday my local HEMA group, Tempered Mettle Historical Fencing, had a guest instructor come to teach a one-day class aimed at “underrepresented groups.” The guest instructor was Kaethe Dundon, “a Chicago-based queer nerd whose major interests are in history, art, and textiles, and of course historical martial arts.” The class was pitched thus:

The primary audience of this workshop includes women, those of other marginalized genders, and those with physical disabilities. Those who are male and able-bodied are welcome to attend – but be aware that your experience will not be the focus of this class, and be ready to primarily take the “losing” role in reps.

I was down with that, so I went. It was a great workshop. A lot of the focus was on stance and footwork, which are two things you can never do too much of.

One member was taking pictures. Trying to be less of a distraction, he switched his camera to “silent,” which turned out to have an odd interaction with the LED lighting in our training space:

The posture with the sword across our shoulders was intended to get us to open our chest, so our arms and shoulders would be where they were supposed to be for longsword.