I have long been a big fan of allegorical figures, such as these two outside the Chicago Board of Trade.

My education in such things was slightly deficient. I mean, every educated person ought to be able to look at such a figure and identify it by the signifiers, the way nearly everybody can recognize Liberty and Justice. These two are only slightly more obscure, so I was able to identify them. (Especially in context—they are particularly appropriate for the Chicago Board of Trade, where commodities are traded.)

Industry, with a gear, anvil, and an anchorAgriculture, with a cornucopia of fruit and corn and with sheaves of wheat

There are many more that I can’t reliably recognize—Fame, Victory, Hope, Time, etc. I’ve looked from time to time to find a nice compact reference with pictures and descriptions, and haven’t found exactly what I was looking for.

In any case, it was fun to see these two, just across the street from the Chicago Federal Reserve Bank, where we had gone to visit the Money Museum—about which I hope to write a post soon.

Many politicians and financial analyst types are suggesting that the Fed should “look through” tariff-induced price hikes. Superficially this makes sense, because a one-time cost increase is not the same thing as inflation. Unfortunately, we know that the results are bad.

The example I’m thinking of is the price shock from much higher oil prices due to the 1973 OPEC oil embargo. As that price shock moved through the economy, first oil prices went up, then gasoline prices went up, but very shortly all prices moved up, because every business faced higher energy costs, and needed to pass at least a fraction of them forward. And then, of course, all the businesses that bought things from those businesses needed to raise their prices further, and workers started demanding higher wages because their costs were going up.

The Federal Reserve tried to “look through” that price shock, not raising interest rates, even though prices were rising. As I say, this makes sense. The one-time price shock will move through the economy, raising many prices by various amounts (depending on how much the inputs for each particular item increase in cost, and the market constraints on price increases for each particular item). Once that all works through the economy, the prices increases should stop.

In fact, raising interest rates could easily make things worse, because the cost of credit is another cost to nearly all businesses, so it’s just another expense that they have to pass on, and it’s a cost to employees, that they’ll want to recover in wage negotiations.

But we know what happened: Inflation rose enough that the Fed eventually decided that it needed to raise interest rates. Higher interest rates hurt the economy, threatening to produce a recession. The Fed cut interest rates to head off the threatened recession, which led to inflation, which led to the Fed raising rates again, etc.

The result was the stagflation of the 1970s, which only ended when new Fed chairman Paul Volker raised rates high enough to produce a severe recession, and then kept them high for long enough to wring the inflation out of the economy.

To me it’s clear that “looking through” the “one-time” price shock of higher tariffs will produce the same result. The Fed can probably mitigate it by holding rates at their current levels until the price shock works its way through the economy (which will probably take a least a year, because many prices (wages, rents, etc.) are only renegotiated annually), and only cut rates after price increases settle back down to close to the Fed’s 2% target.

I assume the Fed governors know this. Do they have the courage to take the right action? Only time will tell.

Let me start by saying that, judging from his previous term, most of what the incoming president says has no particular bearing on what he’s going to do. But I think a few trends look likely enough that it’s worth thinking about the results on the dollar’s value.

The things I’m thinking of are tariffs and tax cuts, which I expect to lead to higher inflation and larger deficits, both of which will lead to higher interest rates.

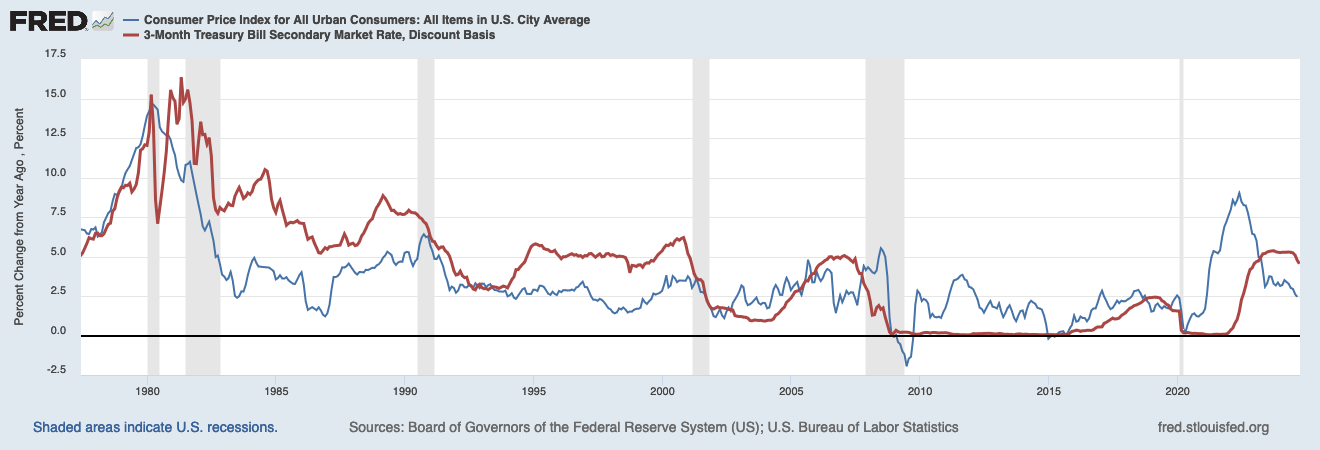

Blue is the historical Inflation rate (CPI vs one year earlier). Red is the historical 3-month T-bill rate (roughly what you could earn in a money market fund). Both are from June, 1977 (when I graduated from high school) through last month.

Tariffs

The president can impose tariffs on his own, with no need for congressional action. Whether we’ll get the proposed 60% tariffs on Chinese goods, or whether that’s just a bargaining chip, I have no idea. But I think some amount of tariff increase will be imposed, which will feed through directly to higher prices.

That’s not to say that tariffs are necessarily bad (although usually they are). But they do feed through to higher prices.

Tax cuts

Tax cuts need to get through Congress. If the Republicans get the House as well as the Senate, it’s highly likely that legislation will preserve the 2017 tax cuts set to expire next year, and probably some additional tax cuts, such as a much lower rate on corporate income. It’s also possible that we’ll see the proposals to cut tax rates on tip income and on overtime pay enacted, although I doubt it. (The incoming president only cares about his own taxes, not about those of random working-class folks.)

The main thing taxes cuts will do is dramatically increase the deficit. The tariffs will bring in some countervailing revenue, but not nearly enough to fill the gap.

Other things that raise inflation and cut revenue

There are all kinds of other proposals that were bandied about during the campaign, such as deporting millions of immigrants, that raise costs both for the government, leading to higher deficits (the labor and logistics both cost money, and not a little) and for employers (they’re employing the immigrants because their wages are lower), which they will try to offset with higher prices.

What this means for our money

Rising costs will feed directly into higher prices, which is going to look like inflation to the Fed, so I think we can expect short-term interest rates (the ones controlled by the Fed) to get stuck as a higher level than we’d otherwise have seen.

At the same time, lower taxes will mean lower government revenues, leading to larger deficits. For years now, the government has been able to get away with rising deficits, but I doubt if the next administration will have as much success in this area. (Why not deserves a post of its own.)

My expectation is that higher deficits will mean higher long-term interest rates, as Treasury buyers insist on higher rates to reward the risks that they’re taking.

So: Higher short rates and higher long rates, along with higher inflation.

What to do

I had already been expecting inflation rates to stick higher than the market has been expecting, so I’d been looking at investing in TIPS (treasury securities whose value is adjusted for inflation). I’m still planning on doing so, but not with as much money as I’d been thinking of, for two reasons.

First, I’d been assuming that money market rates would come down, as the Fed lowered short-term rates. Now that I think short-term rates won’t come down as much or as fast, I’m thinking I can just keep more money in cash, and still earn a reasonable return.

Second, I’d been assuming that treasury securities would definitely pay out—the U.S. has been good for its debts since Alexander Hamilton was the Treasury Secretary. But the incoming president has very odd ideas about bankruptcy. As near as I can tell, he figures the smart move is to borrow as much as possible, and then declare bankruptcy, and then do it again. It worked for him, over and over again. I’m betting that Congress won’t go along with making the United States do the same, but I’m not sure of it.

Of course, if the United States does do that, the whole economy will go down, and my TIPS not getting paid will be the least of my problems.

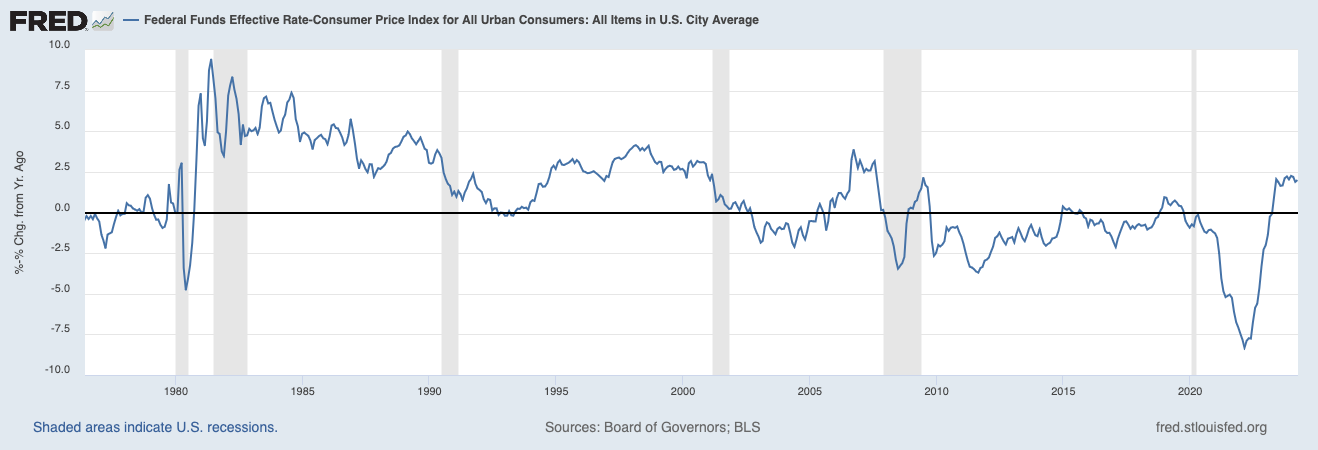

People expect the Fed to cut rates, because they are high. But interest rates are not high:

That’s the real fed funds rate going back to the month I graduated from high school. I’d say a real interest rate of 2.0% to 2.5% is more “normal” than the negative-to-zero rates we’ve had since 2007.

I observed a year ago that post-crisis bank regulation amounted to the Fed admitting that it was a failure, with banks treating reserves like pre-1913 banks treated gold. So I’m pleased to see that at least some Fed officials understand that this is a problem.

it is worth remembering that a principal reason for the Federal Reserve’s creation was to facilitate the movement of reserves when needed from banks with an excess reserve position to those in need of reserves

Why has the Fed been able to produce asset inflation but no price inflation for past 10 years? My guess: lack of union power and globalization are blunting transmission into wages and prices. But I don’t see an easy way to test that hypothesis.

The “gig” economy: all the sorts of work arrangements where you’re not a permanent employee and can’t expect that work one day implies that you’ll have work the next day—freelancing, contracting, temp work, casual labor, and most recently, software-mediated contract work like Uber driver.

These sorts of work have been growing as a fraction of all work. In fact, according to the Bureau of Labor Statistics, in the last ten years contingent workers have gone from being 10% of the workforce to being 16%. In fact,

all of the net growth in aggregate employment in the decade leading up to 2015 can be accounted for by contingent work arrangements, which means there has been no net employment growth in traditional work arrangements.

So this raises the question: Does strong growth in the number of freelancers, on-call temps, and Uber drivers mean that we’re getting closer to maximum employment? Or, that we’re getting further away?

During the debt ceiling crisis back in 2011, I suggested that it would be no big deal if the government just “prioritized” spending so as to match revenues for however long it took Congress to get its act together and raise the debt ceiling. I got some push back on this by people who said I was crazy if I thought that much spending would suffice, but I never thought it would suffice—I was just sure that the result would be so onerous that Congress would knuckle under in no time. I figured that was what the Treasury secretly had in mind.

I’ve changed my mind.

It would have gone like this: The laws are contradictory—Congress sets the tax rates, Congress sets the spending levels, Congress sets the debt ceiling. The poor Treasury, simply doing the best it could in a no-win situation, would hold up pretty much all payments except interest on the debt, judges pay, soldiers pay, and social security. Once payments to major corporations in districts where recalcitrant Congressmen lived got held up, the stalemate would have ended pretty quickly.

I no longer think that’s what’s going to happen. Basically, I’ve come around the view that the Treasury meant what it said when it claimed that its hand were tied: It is legally required to spend the money the Congress has appropriated, whether the money is raised or not.

And I think there’s a solution.

Really, it’s the same solution as the “platinum coin” solution or the “issue scrip” solution, but those solutions are just gimmicks to put a pseudo-legalistic shine on what basically amounts to paying our bills by printing money.

I don’t think there’s any need for the gimmick. I think what the Treasury means to do once the headroom for keeping under the debt ceiling runs out is: Nothing. They’ll just go on writing checks exactly as they’ve been doing.

They’ll stop issuing new debt of course, so there’ll be no new money in their account at the Federal Reserve to pay the checks.

At which point, I’m reasonably sure, the Federal Reserve will just pay the checks anyway—which the Fed can easily do by just crediting the depositing bank’s account. (In other words, printing the money.)

Basically, the Fed would let the Treasury run an unlimited overdraft.

This works on several levels.

First of all, it doesn’t require any reprogramming or rejiggering of the Treasury’s numerous systems for making all the many payments they make every day. (No entity makes more payments than the US Treasury.) That’s good, because any attempt to do so would be problematic at best, and probably catastrophic in the short term.

Second, the people who are being most recalcitrant about raising the debt ceiling are the ones who would be most outraged. (I can just see them frothing at the mouth. Oh noes! Inflation!!1!)

Third, under the current circumstances, it would probably be good for the economy. I’ve pretty much come around to Paul Krugman’s analysis that at the zero bound there is no inflation risk to printing money. Even better, if it did produce some inflation, that might get us up off the zero bound. (I for one would be very pleased to be able to earn a return on my capital.)

A generation ago the Fed would have hated this—bankers used to hate overdrafts in the deepest depths of their bowels. But overdrafts have been so profitable for banks these past 20 years or so, I expect we have a whole generation of bankers who have gotten over it.

As to whether it’s really legal or not, that’s something for the courts to decide. The debt ceiling applies to debt “subject to the limit.” The Fed and the Treasury will just say that, while an overdraft is debt, it’s not debt “subject to the limit.” The debt ceiling will be resolved long before any court case plays out.

The Treasury never admitted to having any contingency plans last time. Their take on it was that not raising the debt ceiling was unthinkable, therefore they would not think about it. But this is the only thing I can think of that could actually play out without chaos. If they weren’t planning on doing this (or something much like it), they’d have done something by now (such as having a dry run of their scheme for prioritizing payments).

Last time, I figured we’d get an 11th hour deal. This time, I think it’s pretty likely that the debt ceiling won’t get raised, and I think the Treasury will actually end up doing this—so I thought I’d share my thinking in case people find it useful.