“Higher Gas Prices Are Hitting Lower-Income Americans the Hardest”

—Latest headline from the petroleum economics journal “Duh!”

“Higher Gas Prices Are Hitting Lower-Income Americans the Hardest”

—Latest headline from the petroleum economics journal “Duh!”

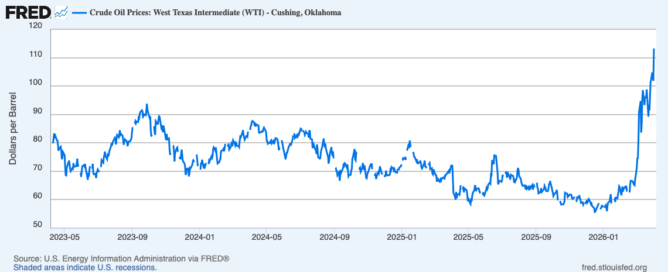

For no reason I can understand, markets seem to think that (with the cease fire with Iran) things are going to return more or less to normal, more or less immediately. This is false. It is not just false, it is so far from the truth that I don’t understand why way more people aren’t panicking.

There are so many problems with oil supply delivery right now—so many more than just the Strait of Hormuz. A lot of oil and gas production infrastructure is gone. A lot of oil and gas distribution infrastructure is gone. Even where the production infrastructure is still there, since there’s no way to ship out what is produced, production is being shut in. Production that has been shut in will take weeks to get started again. And it won’t be started again until it can be delivered.

At the same time, shipments of oil and gas that came out through the Strait just before it was closed, are probably only now reaching their destinations—meaning that it is only now that refineries are finding themselves without their next input for refining. The refining facilities are going to have to shut down. And just like the production facilities, it will take weeks to get them started again. And they won’t be started again until the people who run them foresee reliable, steady deliveries of crude.

These effects are already obvious in the observed spread between spot prices (the cost of a barrel of crude to be delivered right now), which are high (although not as high as I think would make sense), and futures prices (the cost of a barrel of crude to be delivered in a month), which are also high (but not nearly as high as I think would make sense).

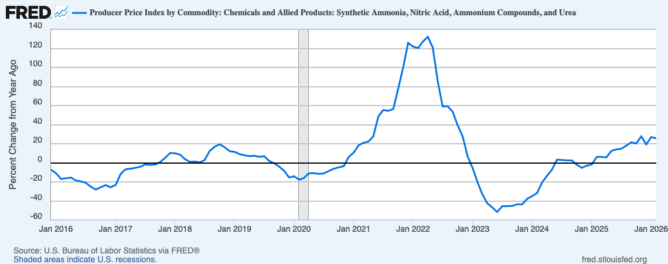

The same is true (with various differences in details) with helium, nitrogen for fertilizer, aluminum, and who knows how many other commodities that used to come though the Strait.

This all matters because the knock-on effects are going to be huge. Higher fuel prices—much higher, and for much longer than the markets are currently anticipating. Higher food prices, due to the shortage of fertilizer reducing food production, especially of corn—which is a major input to both meat production and to ethanol production, meaning another way it feeds-through the higher energy prices. Higher helium prices feed through to shortages of computer chips—which were already under strain due to AI-related data-center demand.

In the background of all these are Trump’s tariffs from a year ago, the impact of which was eased in many different ways (the pause, various rate cuts, firms stocking-up ahead of the imposition of the taxes, the supreme court decision ruling that the worst of them were illegal), all of which delayed the main impacts for months. For some reason, the markets seem to think that those impacts would quit showing up in comparison to the year-ago numbers (since the tariffs were announced one year ago), but in fact are probably only now fully showing up in reported numbers.

My take on all this is that every aspect of the economy is going start getting bad, and then going on getting worse. The getting-worse phase will go on at least for months and months, and very possibly for a year or two or three.

Inflation spiked up to 3.3% last month, but that is only the start. That’s just the energy-price spike. As soon as those effects feed through to other prices, they’ll all go up. And as soon as those high prices start forcing people to cut back on other spending, we’ll see at least a recession, and very possibly worse than that. And that’s all before actual shortages or fuel and food start impacting every aspect of people’s lives.

Oh, and as I’ve said before: Don’t imagine that having some idea about what things are going to be higher-priced or in short-supply gives you the sort of insight that will let you invest to make money off these circumstances. The real-world impact of these things are going to be chaotic enough that any particular investment could go very badly wrong, even if your understanding of the general direction of events is correct. And, of course, the government is going to trying to protect their supporters (oil companies and tech billionaires, mostly) so they may well be bailed out. Any investments that suppose that things will go badly for them in particular may well go spectacularly awry.

Recent news is that a contingent of ground forces have arrived in Iran. The markets still seem expect that Trump will chicken out (which seems likely) and that things will return to normal in the Gulf (which seems very, very unlikely).

My most hopeful guess at this point:

All my other guesses are similar, except that my scenario is preceded by a step 0 in which a bunch of U.S. soldiers and marines are killed while failing to reopen the Strait.

Many politicians and financial analyst types are suggesting that the Fed should “look through” tariff-induced price hikes. Superficially this makes sense, because a one-time cost increase is not the same thing as inflation. Unfortunately, we know that the results are bad.

The example I’m thinking of is the price shock from much higher oil prices due to the 1973 OPEC oil embargo. As that price shock moved through the economy, first oil prices went up, then gasoline prices went up, but very shortly all prices moved up, because every business faced higher energy costs, and needed to pass at least a fraction of them forward. And then, of course, all the businesses that bought things from those businesses needed to raise their prices further, and workers started demanding higher wages because their costs were going up.

The Federal Reserve tried to “look through” that price shock, not raising interest rates, even though prices were rising. As I say, this makes sense. The one-time price shock will move through the economy, raising many prices by various amounts (depending on how much the inputs for each particular item increase in cost, and the market constraints on price increases for each particular item). Once that all works through the economy, the prices increases should stop.

In fact, raising interest rates could easily make things worse, because the cost of credit is another cost to nearly all businesses, so it’s just another expense that they have to pass on, and it’s a cost to employees, that they’ll want to recover in wage negotiations.

But we know what happened: Inflation rose enough that the Fed eventually decided that it needed to raise interest rates. Higher interest rates hurt the economy, threatening to produce a recession. The Fed cut interest rates to head off the threatened recession, which led to inflation, which led to the Fed raising rates again, etc.

The result was the stagflation of the 1970s, which only ended when new Fed chairman Paul Volker raised rates high enough to produce a severe recession, and then kept them high for long enough to wring the inflation out of the economy.

To me it’s clear that “looking through” the “one-time” price shock of higher tariffs will produce the same result. The Fed can probably mitigate it by holding rates at their current levels until the price shock works its way through the economy (which will probably take a least a year, because many prices (wages, rents, etc.) are only renegotiated annually), and only cut rates after price increases settle back down to close to the Fed’s 2% target.

I assume the Fed governors know this. Do they have the courage to take the right action? Only time will tell.

Some financial commentators are suggesting that the hit to the economy from the new tariffs will push the Fed to lower interest rates, but I don’t see it. The tariffs will push up prices, so the Fed will feel it needs to stick with higher rates for longer.

The result will be exactly as I forecast months ago: the coming stagflation.

A group of friends and I agreed last week that the most likely result of the most likely policies coming out of this administration is stagflation.

Talking about it reminded me of the Wise Bread post I wrote All about stagflation, so I re-read that. I think has held up pretty well, even though circumstances (financial crisis followed by a pandemic) meant that things didn’t play out as I’d expected. Even so, I think the analysis of how to produce a stagflation is right on: raise interest rates to bring down inflation, but then panic when it’s clear that you’re in danger of producing a recession and cut rates before you’ve gotten inflation under control; repeat until you have high inflation and a recession.

That is, stagflation is usually the result of a timid Fed, that’s afraid to do its job.

The thing is, the policies that I see coming (tariffs and tax cuts) will produce stagflation even if the Fed does a great job. The tariffs directly raise prices, and the tax cuts (through increased deficits) raise interest rates, producing a recession.

In the Wise Bread article I warn that it’s tough to position your investments for stagflation. The reason is that inflation makes the money worth less (helping people with debts, but hurting people with money), while the recession hurts people with debts and people with investments.

Upon reflection though, I don’t think it’s quite that bad. In fact, it’s really just regular good financial advice:

Basically: live within your means and stay liquid.

Let me start by saying that, judging from his previous term, most of what the incoming president says has no particular bearing on what he’s going to do. But I think a few trends look likely enough that it’s worth thinking about the results on the dollar’s value.

The things I’m thinking of are tariffs and tax cuts, which I expect to lead to higher inflation and larger deficits, both of which will lead to higher interest rates.

The president can impose tariffs on his own, with no need for congressional action. Whether we’ll get the proposed 60% tariffs on Chinese goods, or whether that’s just a bargaining chip, I have no idea. But I think some amount of tariff increase will be imposed, which will feed through directly to higher prices.

That’s not to say that tariffs are necessarily bad (although usually they are). But they do feed through to higher prices.

Tax cuts need to get through Congress. If the Republicans get the House as well as the Senate, it’s highly likely that legislation will preserve the 2017 tax cuts set to expire next year, and probably some additional tax cuts, such as a much lower rate on corporate income. It’s also possible that we’ll see the proposals to cut tax rates on tip income and on overtime pay enacted, although I doubt it. (The incoming president only cares about his own taxes, not about those of random working-class folks.)

The main thing taxes cuts will do is dramatically increase the deficit. The tariffs will bring in some countervailing revenue, but not nearly enough to fill the gap.

There are all kinds of other proposals that were bandied about during the campaign, such as deporting millions of immigrants, that raise costs both for the government, leading to higher deficits (the labor and logistics both cost money, and not a little) and for employers (they’re employing the immigrants because their wages are lower), which they will try to offset with higher prices.

Rising costs will feed directly into higher prices, which is going to look like inflation to the Fed, so I think we can expect short-term interest rates (the ones controlled by the Fed) to get stuck as a higher level than we’d otherwise have seen.

At the same time, lower taxes will mean lower government revenues, leading to larger deficits. For years now, the government has been able to get away with rising deficits, but I doubt if the next administration will have as much success in this area. (Why not deserves a post of its own.)

My expectation is that higher deficits will mean higher long-term interest rates, as Treasury buyers insist on higher rates to reward the risks that they’re taking.

So: Higher short rates and higher long rates, along with higher inflation.

I had already been expecting inflation rates to stick higher than the market has been expecting, so I’d been looking at investing in TIPS (treasury securities whose value is adjusted for inflation). I’m still planning on doing so, but not with as much money as I’d been thinking of, for two reasons.

First, I’d been assuming that money market rates would come down, as the Fed lowered short-term rates. Now that I think short-term rates won’t come down as much or as fast, I’m thinking I can just keep more money in cash, and still earn a reasonable return.

Second, I’d been assuming that treasury securities would definitely pay out—the U.S. has been good for its debts since Alexander Hamilton was the Treasury Secretary. But the incoming president has very odd ideas about bankruptcy. As near as I can tell, he figures the smart move is to borrow as much as possible, and then declare bankruptcy, and then do it again. It worked for him, over and over again. I’m betting that Congress won’t go along with making the United States do the same, but I’m not sure of it.

Of course, if the United States does do that, the whole economy will go down, and my TIPS not getting paid will be the least of my problems.

Looked at properly, inflation is the money getting less valuable, which shows up as rising prices. It’s opposite, deflation, is the money getting more valuable, leading to falling prices. Something that used to be very obvious, but has perhaps become less so, is that inflation sucks if you have money, whereas deflation sucks if you owe money.

TL;DR version: You can reverse inflation, as long as you’re willing to grind into the dust everyone who owes money, making them work more and more, to earn less and less, to pay back debts that get higher and higher (because the dollars it takes to pay them off are getting more and more valuable). Society has done that many times in the past. Sometimes it works out okay; other times it produces terrible impoverishment of ordinary people, leading to social unrest.

The rest of this post looks at this in a bit more detail. I was prompted to write it because recent polls have suggested that young folks—Millennials and Gen-Z—continue to be unhappy about inflation, even though the inflation rate is down a lot. When you talk to these people, it turns out what they’re unhappy about is not inflation but rather prices: They remember what things used to cost, and they cost more than that now, which they find annoying, even if the price has largely quit going up. (And of course prices change all the time, so some prices are always going up.)

Older folk—people who lived through the inflation of the late 1970s and early 1980s—have a different perspective on that, partially because their parents and grandparents lived through the Great Depression.

Basically, they remember what happens when you try to push prices back down to what they were before a period of inflation.

There’s a sense among the “hard money” types that inflation is impossible when the currency is backed by gold, but this is false. There is often inflation under a gold standard, but it (often) ended up getting undone, meaning that looked at from the perspective of a century, it looks like there wasn’t much inflation. And indeed there wasn’t much inflation on average.

This was especially true during the heyday of the gold standard, roughly the 18th and 19th centuries. In 1816 the pound sterling was defined as 113 grains of pure gold, where it remained until 1931. (Before that it was defined as 5,400 grains of silver—about a pound of silver, hence the name a pound sterling—but in terms of value it was a similar amount of purchasing power.)

A big part of the reason that people remember the gold standard fondly is that it worked pretty well, especially for people who had money. With stable prices, it was even possible to value land not at a market price (because who would sell land?) but at the income that land would produce—an income that would remain stable for generations at a time.

However, as I said, there was still inflation. Inflation came from many sources, but two important ones: new discoveries of gold, and war. When the quantity of gold increased—as during the 1840s and 1850s when large amounts of gold were found in California and Australia—the rising quantity of gold (i.e. money) would produce inflation just like rising quantities of money produce inflation now. The other common source of inflation was war, because paying for a big war without inflation is almost impossible.

For example, there was a big inflation in the U.S. during the Civil War, when the Federal Government printed “greenbacks” to pay for the costs of the war. (The Confederates did the same, but as they lost the war their Confederate dollars ended up being worthless.) Dollars, on the other hand, were gradually revalued, with greenbacks gradually being withdrawn from circulation producing a grinding deflation that went on for more than a decade.

Like always in economics, there were other things going on at the same time. Industrialization was going on at the same time, meaning that things produced by industrial firms were getting cheaper, leading to deflation, while gold discoveries were leading to an increase in the supply of gold (= money) leading to inflation.

On balance there was deflation, meaning that people who had money were getting richer, while people who owed money were getting poorer. As long as that happens only in a small way, and as long as people sense that it’s “fair”—that nobody is cheating the system to take unfair advantage—it’s kinda nice. If you don’t owe money (and most people didn’t, because there were no credit cards, and virtually no student loans), then whatever meager savings you had got gradually more and more valuable. At the same time, wages tended not to drop (for the same reasons that wages tend not to drop these days as well), so somebody with a job ended up gradually better and better off.

Of course rich people got vastly more well off, so they loved it. The main people who hated it were farmers and small businessmen, because they generally needed to borrow money (to buy seed or raw materials), so they were constantly screwed by the fact that the money they had to pay back was worth more than the money they’d borrowed.

I started this post meaning to suggest that “kids these days” just didn’t understand the dynamics of deflation, But upon reflection, I think there’s another layer to it. Kids these days (as opposed to the Gen-X kids who trusted their parents and guidance counselors, and borrowed as much money as necessary to go to the best school they could get into) don’t owe so much money, so they’re not in the position of being utterly screwed by deflation. Many of them may be in the position of ordinary people in the great post-Civil War deflation, who ended up doing pretty well, with their wages or salary rising in value, while industrialization and globalization helps hold down prices.

The fact is, though, that deflation can absolutely destroy a generation of ordinary people. After WW I, for example, Britain, having funded the war through inflation, decided to return to the pre-war gold parity, which required a grinding deflation that lasted until 1929—great for people with money, bad for people without, devastating for people with debts. France decided instead to revalue, punishing people with money, coddling people with debts (which has its own downsides in terms of social disruption). German, the loser of WW I, saddled with debts denominated in gold, made a valiant effort to pay them back, giving up and starting WW II only when that proved utterly impossible.

The lesson of that period, understood by pretty much everybody from the 1940s through the 2000s, was that the best thing to do after a period of inflation was to bring the inflation rate back down near zero, but accept the price increases that had already happened. (If the inflation rate is brought back down to, let’s say, 2%, prices will be generally stable. The slight remaining inflation will be barely noticeable, hidden amidst the ordinary rise and fall of prices due to changes in fashions, technological improvements in the means of production, depletion of resources, etc.)

It’s very interesting to see young folks returning to the instincts of the 18th and 19th century, thinking the prices should go back to what they were before the inflation. It goes very much against what I learned as an economics student, but who can say that what I learned was right and that their instincts are wrong?

Seems like a situation of “time will tell.”

Sources:

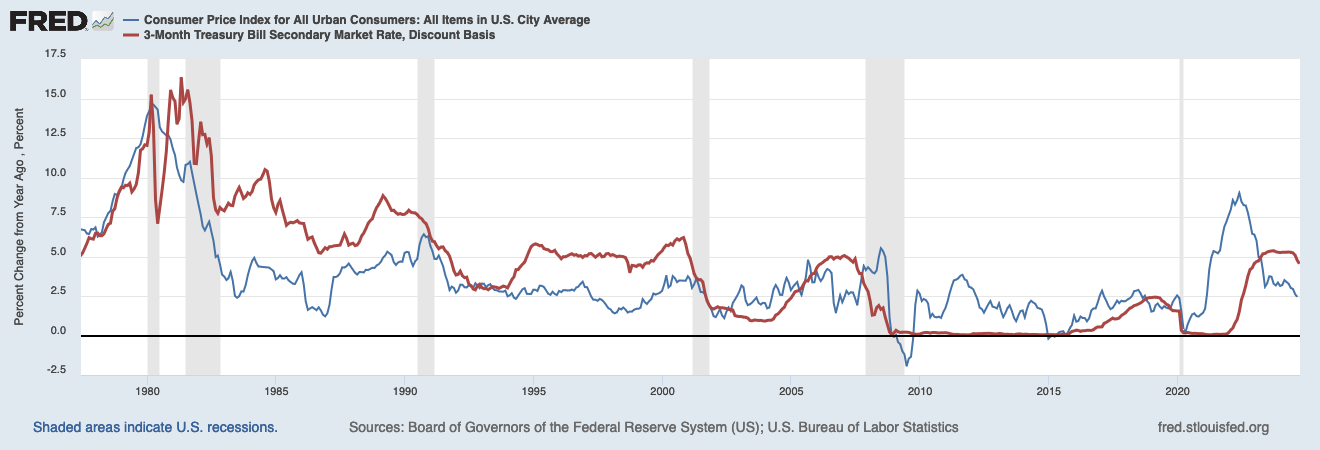

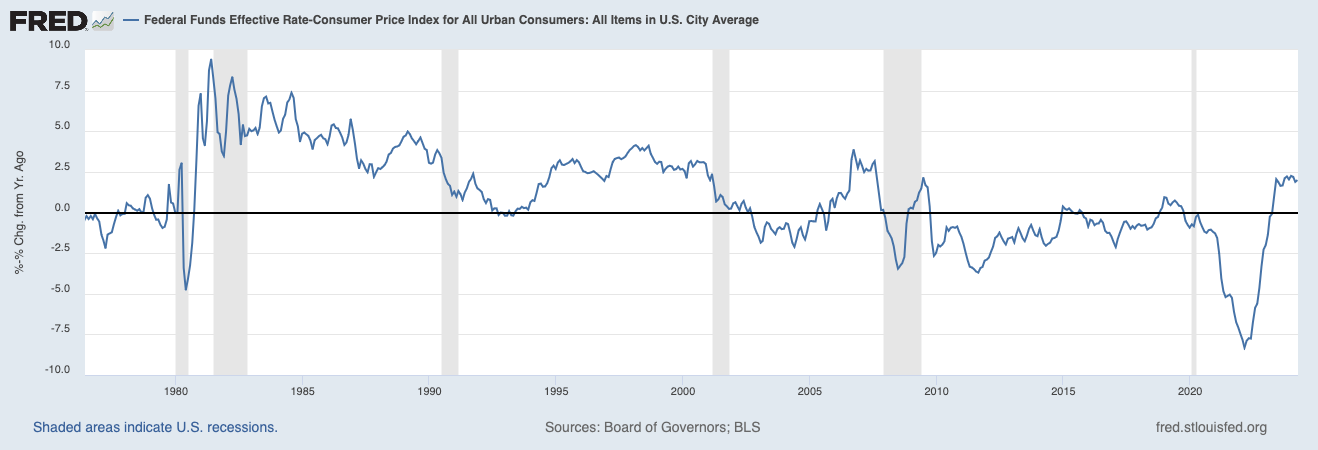

People expect the Fed to cut rates, because they are high. But interest rates are not high:

That’s the real fed funds rate going back to the month I graduated from high school. I’d say a real interest rate of 2.0% to 2.5% is more “normal” than the negative-to-zero rates we’ve had since 2007.

Inflation and a declining standard of living are two different things. Inflation is when the money becomes less valuable, resulting in rising prices. But when a whole society becomes poorer, it can look like inflation, because prices may rise, but it’s not the same thing.

“Despite the Bank of England’s efforts so far, there is accumulating evidence that inflation will be harder to stamp out than previously expected. In the past week, data has shown that pay in Britain has increased faster than expected, inflation in the services sector has accelerated and food inflation is still near the highest level in more than 45 years.”

https://www.nytimes.com/2023/06/22/business/economy/bank-of-england-interest-rates-inflation.html?smid=url-share

To my eye, viewed from over here, that looks less like inflation and more like a falling standard of living—largely caused by Brexit. If you block immigration, of course wages are going to go up. If transporting stuff across the border takes longer and is more expensive and difficult, of course food is going to be more expensive. That’s not inflation. That’s reducing everyone’s standard of living by raising actual costs.

It looks similar, because the symptom tends to be rising prices, but they’re two different things. If the problem is inflation, then raising interest rates (by reducing the rate of growth in the money supply) will probably help. But if the problem is a declining standard of living, then it’s probably not going to help. Higher interest rates will just be yet another expense (like border controls) that flow through to making everything cost more.