A few weeks ago, back before the Iran war heated back up, The Economist wrote a mia culpa, explaining why they’d gotten it wrong about the war being an economic disaster. Briefly, while the MOU was holding up, I was tempted to write my own.

Like The Economist editors, I had thought back in April that Things are amazingly more bad than markets seem to think, but by the beginning of June, it was looking like maybe the risk of catastrophe had eased.

I didn’t write a mia culpa. To be fair, part of that was just laziness. But part of it was looking at things and thinking I was still right. Maybe between some demand destruction and some dribs and drabs of oil getting through the strait, world markets had found a new equilibrium that wasn’t nearly as bad as I’d expected. But I didn’t think so.

The Economist thought so. They thought they’d gotten it wrong for two reasons:

First, we thought that America and Iran would hold out against a deal to reopen the Strait of Hormuz: America because Mr Trump deludedly thought he held the whip hand, Iran because its regime knew its people could be made to endure more pain. In fact, facing the fury of American motorists, Mr Trump all but folded, preventing a disaster. Since the two parties struck a provisional deal in June, enough oil has been getting out of the Gulf to reassure markets that supply is coming back online, even if the future of the strait remains uncertain.

Our second oversight was, like others, not anticipating the staggering degree to which China would be able to slash its oil imports. Crude imports are 5m barrels a day lower than a year ago, despite the fall in prices. China has cut its demand and shored up supply. Its oil reserves are opaque—many barrels are hidden from satellites underground, and there is a blurred line between official reserves and corporate inventories. But they have been shown to be a powerful buffer.

I pretty much bought their second point. China had produced a truly fantastic amount of demand destruction, and had done it with minimal impact on their own economy, by largely shifting the impact onto people in other countries who had bought their oil distillates, before China prohibited exports. They could probably keep that up indefinitely, removing their demand from the world market.

That first point, though, I found doubtful. I mean, yes, Trump always chickens out, which is why we got the MOU and the briefly partially reopened strait. But I think they were wrong in thinking that Iran would go along with what Trump wanted, or that Trump could settle for what Iran would (obviously) want to do. They tried to paper over the cracks for a few weeks. I mean, I believe Trump settling for whatever Iran did and pretending it was a victory was a thing that could happen. But I’m not surprised it didn’t work out. Too many other people in the U.S. government were simply unwilling to let Trump leave the strait in Iran’s hands. And, although oil prices were coming back down, they were not on a trajectory that would improve the Republican’s chances in the midterms.

So, I think The Economist was right in the first place, and wrong to imagine that Trump and Iran could agree that “preventing a disaster” was something they could do.

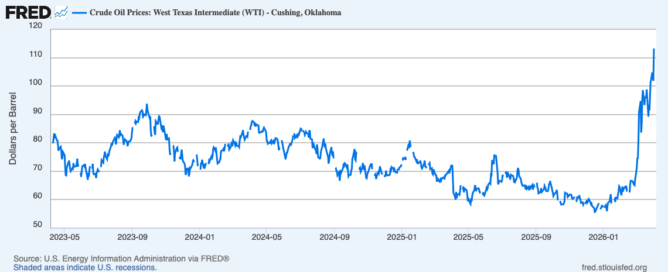

The oil price graphic above is already out of date. It shows yesterday’s closing price, and things have gotten worse already today. Brent crude is over $100 as I wrap up this post.